Executive summary

Between January and March 2026, third-party CS2 skin markets showed stable operations with very large inventory depth, tens of millions of active owners, and steady daily item churn. A composite market index near ~1142 acted as a balancing line for the quarter: not a perfect oracle, but a useful pulse check when read together with volume, value, and participation metrics.

This article summarizes the segment structure (rifles vs. knives vs. gloves vs. stickers vs. cases), highlights what typically drives liquidity, and ends with a practical risk framework for individual traders.

Market overview

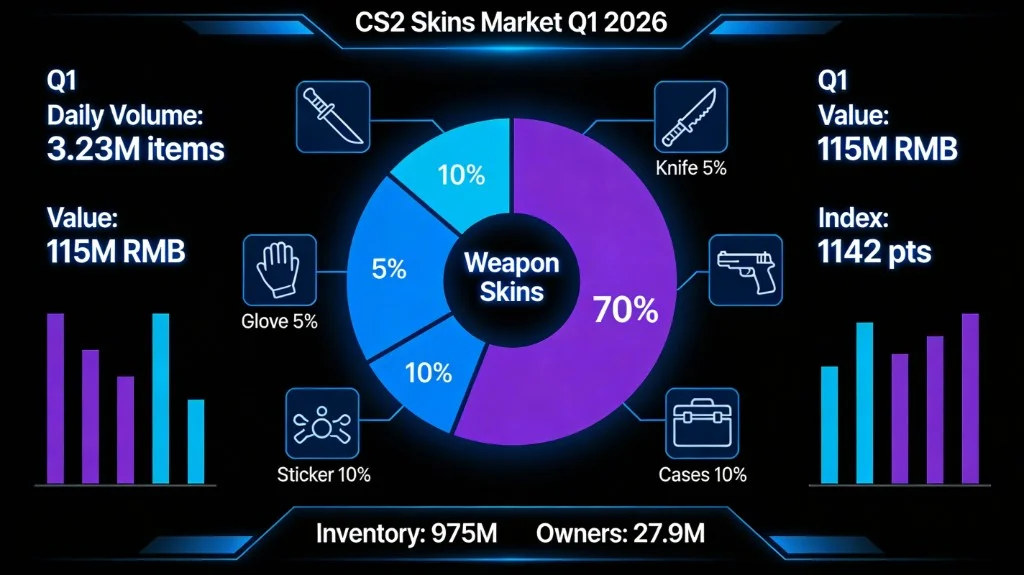

Inventory scale reached roughly 975.6 million cosmetic items in Q1 2026, supported by about 27.9 million distinct owners—evidence of a deep, globalized player economy layered on top of Steam Workshop supply.

Reported daily transaction volume averaged about 3.23 million items (up roughly 4% month-over-month in the series this research drew from), while transaction value averaged about 115 million RMB per day, with a recent print near 127.3 million RMB (down about 5.01% month-over-month). That divergence—more units, softer headline value—often appears when cheaper, high-churn skins carry volume while premium tiers reprice.

New inventory additions averaged about 26.72 million RMB per day (roughly 103 million items), down about 8.38% month-over-month, which can indicate supply normalization after heavier inflows, changes in unboxing cadence, or shifts in what traders choose to list.

The market index printed near 1142.29 with a small daily gain (~0.33%) after a short streak of declines, while online users averaged about 1.6 million (up ~10.47% day-over-day in the snapshot), which tends to support tighter spreads and faster matching when sustained.

How to read this responsibly: third-party statistics can differ by venue, API coverage, and FX reporting. Use the numbers here as structured context, then confirm execution prices on the venues where you actually trade—see our guide to third-party CS2 marketplaces.

Segment analysis

Weapon skins (volume engine)

Weapon skins remained the default liquidity layer: commonly cited as >70% of daily transaction volume (>2M items/day in the underlying sample) and a large share of total value. Factory New wear showed elevated participation (around 30% of transactions in the referenced window), consistent with collectors and flippers competing for clean floats.

The AK family is the classic “workhorse + flex” line in many regions—if you want a liquid reference point for what “busy” looks like in rifles, is frequently treated as a high-churn benchmark in community trading discourse.

Knife skins (premium convexity)

Knives led the premium tail: average price momentum in the sampled series landed near +2.14%, above the broad market average, with high average listing prices in RMB terms. Collections and finish rarity often amplify non-linear repricing—great in upswings, painful if liquidity thins.

For a recognizable high-end example tied to finish hype, many traders anchor sentiment around blades like —use it as a category illustration, not a buy recommendation.

Glove skins (concentrated value)

Gloves remained structurally scarce relative to rifles: under ~1% inventory share but a large contribution to transaction value (on the order of ~15% in this dataset), with concentrated ownership (under ~5% of users). Daily glove volume stayed above 10,000 items with drawdowns typically contained within about 1% in the quoted window—consistent with sticky supply and collector-grade bid depth.

remains a cultural anchor for neon, high-tier loadouts and is often used as shorthand for “gloves as a portfolio sleeve.”

Stickers (event beta)

Stickers behaved like event-driven options: strong leaderboard presence in Q1 heat metrics, with some new tournament-linked stickers up >5% in the measured interval while total sticker inventory stayed under ~10 million items. The pattern is familiar—narrative spikes, then selective retention of truly scarce crafts.

If you are new to how Majors reprice paper supply, start with how CS2 Majors affect prices.

Cases and consumables (supply chain link)

Case inflows averaged about 1.03 million new units per day (down ~8%), while consumption near 500k units/day helped channel ~26.72 million RMB in “new value” creation (about 20% share in the decomposition used here). Cases connect unboxing demand, trade-up inputs, and liquidity recycling across the rest of the economy.

Key trends and data comparison

| Segment | Daily volume share | Avg gain/loss (directional) | Inventory share | Q1 2026 characteristics |

|---|---|---|---|---|

| Weapon skins | 70%+ | +2% to +4% | Highest | High circulation, broad price ladder |

| Knife skins | <5% | ~+2.14% | Low | High unit price, collection-led moves |

| Glove skins | <5% | within ~−1% | <1% | Concentrated owners, value-heavy |

| Stickers | Medium | +5%+ (event windows) | <10% | Theme/tournament narrative sensitivity |

| Cases | 10%–20% | ~−8% on new inflows | Medium | Supply adjustment + steady consumption |

The ~1142 index level is best interpreted as cross-segment equilibrium: rifles keep the market “moving,” while knives/gloves can lead repricing when risk appetite shifts.

Risks and outlook

- Supply rhythm: slower additions can support prices, but they can also precede volatility if demand softens at the same time.

- Policy and mechanics risk: Valve rule changes historically remap liquidity overnight; premium segments (knives/gloves) can overshoot on headlines.

- Value vs. volume: rising item counts with falling headline value can signal mix shift—monitor whether the decline is broad-based or composition-driven.

For risk management in peer-to-peer flows, revisit how to trade CS2 skins safely. If you are thinking in portfolio terms, pair this macro view with long-term vs. short-term CS2 investments.

Base case for Q2 2026: continued layered market structure—rifles as the liquidity backbone, knives/gloves as convexity sleeves, stickers as event beta, and cases as the connector. Watch index trend, online participation, and listing inflow as early tells.